Article | 7 minutes read

How do you build gambling regulations that protect players without driving them offshore? Ontario and Germany offer two very different answers.

Both jurisdictions overhauled their online gambling markets within a year of each other. Yet the regulatory models they chose could hardly be more different. Ontario opted for market liberalization, competition, and high channelization. Germany opted for a more restrictive framework that prioritizes player protection and purposefully aims to make gambling less attractive.

Based on nearly four years of operating data and insights from iGaming.com CEO Prof. Dr. Andreas Ditsche at the SBC Summit Canada, the evidence suggests Ontario’s model is producing stronger channelization results.

Ontario’s competitive online gambling market opened in April 2022. Its dual-agency structure separates regulation from commercial management. The Alcohol and Gaming Commission of Ontario (AGCO) sets and enforces the rules. iGaming Ontario (iGO), a subsidiary of the AGCO, contracts directly with private operators that want to run in the province.

The framework borrowed elements from the UK Gambling Commission, Sweden’s Spelinspektionen, and the Danish Gambling Authority. All of those jurisdictions have prioritized channelization over hard supply caps.

The political logic is straightforward: bring existing demand into the licensed market, tax it, and use the proceeds to fund player protection. Provincial messaging at the SBC Summit Canada 2026 reinforced the point. Ontario’s gaming minister argued that growth and player protection are compatible, not competing, goals.

Germany’s framework is broadly anythe inverse. The Interstate Treaty on Gambling 2021 established the country’s first unified online regime, supervised by the Joint Gambling Authority of the Federal States (GGL). Many of its rules are designed to limit gambling activity or make legal products less attractive:

The monthly deposit limit is enforced via a centralized single-customer-view database. That means the same player cannot exceed that ceiling by splitting bets across operators. Those product-side restrictions sit alongside a marketing framework far tighter than Ontario’s and a turnover-based tax that compresses operating margins.

As black market analysis has shown, every restrictive regime faces the same structural risk. If the legal product becomes less attractive than unregulated alternatives, migration to offshore sites accelerates. The protections apply only to the share of demand that remains within the licensed market.

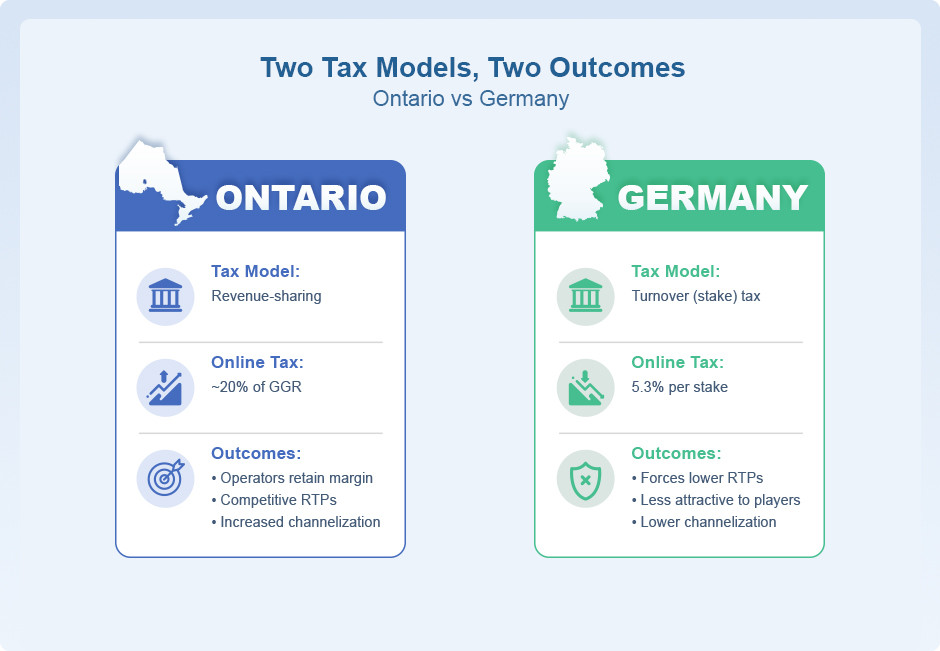

Tax design is where the two philosophies diverge most significantly.

In Ontario, operators pay iGO a revenue share based on gross gaming revenue (GGR), which is wagers minus winnings paid out. Public reporting puts the effective rate around 20% of GGR, in line with established European liberal markets. A GGR-based system enables operators to retain enough margin to offer competitive return-to-player (RTP) rates and marketing spend.

Germany flipped the arithmetic. Online slots and sports betting carry a 5.3% levy on gross stake volume, not on retained revenue. Because the charge is assessed on what players wager rather than what operators keep, German licensees often need to set lower RTPs to break even.

RTP is one of the clearest differences players notice when comparing licensed sites with offshore alternatives. Industry associations argue that the tax structure is the root cause of Germany’s channelization shortfall.

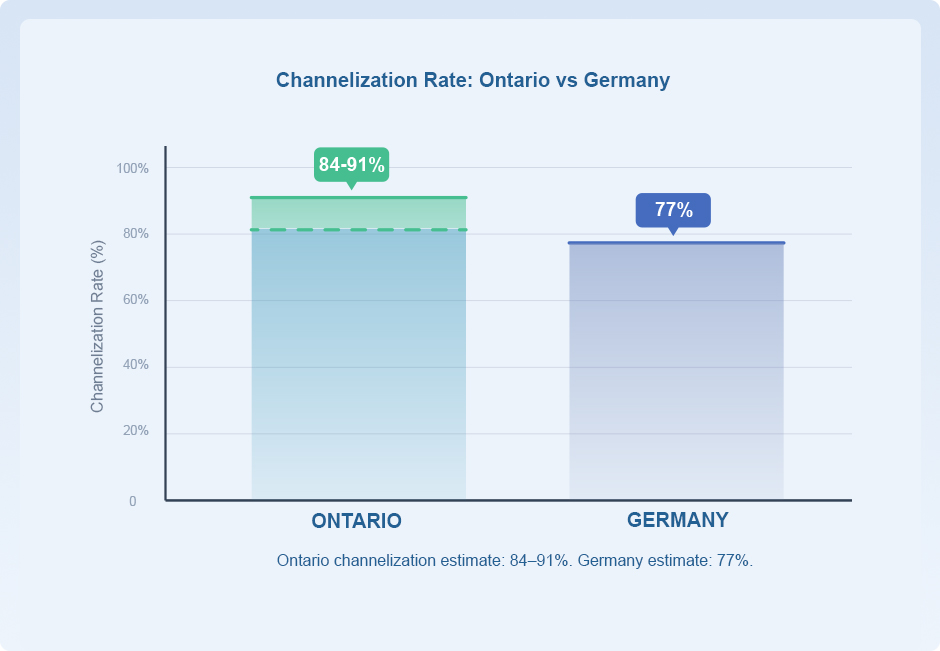

Channelization — the share of money wagered through licensed channels rather than offshore — has emerged as the clearest summary metric for regulatory effectiveness. Higher figures mean more of the market sits inside the rules; lower figures mean the rules apply to a shrinking slice of total activity.

Ontario reports figures at the upper end of what regulated online markets have achieved internationally. The AGCO has commissioned Ipsos research putting the share of Ontario adults who play exclusively on regulated sites at 83.7%. Meanwhile, provincial officials have cited a 91% channelization rate in stage remarks at the SBC Summit Canada.

Together, those readings put Ontario’s regulated share between roughly 84% and 91%. The province processed approximately CAD 82.7 billion in online wagers during the 2024/25 fiscal year, generating around CAD 2.9 billion in GGR.

In contrast, Germany’s headline channelization figure is approximately 77%, set out in a 2024 study commissioned by the GGL. That figure is contested. The Deutscher Online Casinoverband (DOCV) and other industry groups argue that the real figure is closer to 50%.

Within the online slots segment specifically — which is the product hit hardest by the €1 stake cap and turnover tax — channelization is reportedly as low as 20–40%. The GGL’s own 2024 black market study estimated illegal operator GGR at €547 million, a 17% year-on-year rise that German operators have publicly called “too conservative.”

The debate over Germany’s channelization matters because broad national figures can obscure what is happening at different levels.

The 77% headline reads very differently once you note that sports betting channelization sits around 60–70% while online slots, by industry estimates, run at 20–40%. This creates a difficult policy problem: the product most associated with gambling harm may also be the one Germany is struggling most to keep inside the licensed market.

Ontario’s 91% figure appears impressive, but it captures the share of players using regulated sites, not the share of stakes coming from the highest-spending cohort. As earlier comparative work has shown, revenue concentration among a small share of players is a structural feature of every regulated online market that has been measured. That means the prevention strategy must focus on the high-stakes minority, regardless of the regime.

Three structural takeaways for regulators:

The figures below summarize the two markets side by side. Population and GDP figures come from public economic data. Market and regulatory metrics are sourced from published reports by regulators and industry associations, including iGO, AGCO, and GGL.

| Metric | Ontario | Germany |

|---|---|---|

| Population | Approx. 16.1 million | Approx. 84 million |

| GDP | Approx. CAD 1.18 trillion | Approx. €4.3 trillion |

| Online Market Launch | April 2022 | July 2021 |

| Regulatory Model | Liberal competitive market | Restrictive federal-state model |

| Online GGR | CAD 2.9 billion | Approx. €3.5 billion |

| Wagers | CAD 82.7 billion | Estimated > €100 billion |

| Wagers per Capita | Approx. CAD 5,140 | Approx. €1,200–1,500 |

| Tax Base | GGR | Turnover (stake) tax |

| Online Tax | Approx. 20% of GGR | 5.3% per stake |

| Channelization Rate | 84–91% | Approx. 77% |

| Political Priority | Market attractiveness | Prevention |

The per-capita wager comparison is one of the most striking lines in the table. Ontarians wager more than twice as much per head as Germans, despite Germany’s online market being older and serving a much larger population.

The gap is unlikely to be explained solely by consumer demand. German residents continue to gamble online, but much of that activity is happening outside the sector the GGL supervises.

Ontario is not the only liberal market with strong channelization, but it now appears to be matching or outperforming more established European peers. Sweden, often cited as the original liberal-market reference, has stabilized at around 85%.

The Netherlands sits closer to Germany on the regulatory spectrum. It has seen its revenue-based channelization slip toward 53% under a moderately restrictive framework that includes affordability checks and deposit limits.

For policymakers weighing product attractiveness against prevention, two practical implications are emerging:

Current evidence points to a clear lesson: achieving high channelization is difficult without a legal product that players actually want to use.

Ontario and Germany now sit on opposite sides of that argument. Ontario built a competitive market with player protection layered into the licensed system. Germany built a restriction-led model that puts harm prevention first, even when that makes the regulated product less attractive.

Roughly four years in, the channelization data favors Ontario’s approach. The harder question is whether either model does a better job of reducing gambling harm in absolute terms. That will require several more years of post-regulation data on gambling-related harm. For now, the Ontario–Germany comparison is one of the clearest case studies regulators have when weighing market attractiveness against prevention.