Article | 9 minutes read

Legal online gambling in the Netherlands has stopped growing. Gross gaming revenue (GGR) hit €602 million in the second half of 2025, almost identical to the €600 million in the previous half-year. The figures come from the Spring 2026 Monitoring Report published on April 16 by the Dutch Gambling Authority (Kansspelautoriteit or KSA).

That flat result stands out against a European market that grew roughly 11% in 2025 compared with 2024, according to H2 Gambling Capital figures cited in the report. More striking is that legal account numbers are climbing, but actual player numbers are not. Players are spreading across multiple operators, possibly to work around strict deposit limits and proof-of-income checks.

The report also noted that player-based channelization remains high, with roughly 91% of Dutch gamblers playing exclusively at licensed sites. However, the KSA estimates that revenue-based channelization is much lower, at around 53%, suggesting that more of the wagered money is flowing to unlicensed sites.

Dutch online GGR has held at around €100 million per month through 2025, after a steep drop from the 2024 peak. Compared with 2024, revenue is down roughly 18%. Only 27 of 31 licensed operators were actively running games in December 2025, while the others had not yet launched their services. Also, one licensee exited the market during the reporting period.

Legal operators have also lost pricing power. The top three providers held between 30% and 40% of the market at the end of 2025, down from a 40% to 50% range six months earlier. That follows a broader trend of market concentration easing as more licensees compete for the same player base.

Two segments dominate the legal market. Casino games against the house, including virtual slots, made up 78% of GGR. Sports betting accounted for another 20%. Player-versus-player games such as poker and bingo, along with horse racing, accounted for less than 2% of total revenue.

Licensed operators recorded 1.38 million active accounts per month in the second half of 2025, up from 1.29 million in the first half of the year. Yet the estimated number of active players fell from 850,000 in H1 to roughly 810,000 in H2. Because not every player is active each month, the monthly number was lower, at about 500,000 in H2.

The KSA links that gap to multi-accounting. A Dutch player used 3.2 licensed operators on average in the second half of 2025, up from 3.0 and 2.8 in the prior 6-month periods. Regulators suspect some players are opening additional accounts to sidestep net deposit limits introduced in October 2024.

The Netherlands has long measured regulatory success through channelization, the share of gambling activity happening on licensed sites. By that measure, results are mixed.

The Spring 2026 Monitoring Report shows that player-based channelization remains high. Around 91% of Dutch online gamblers play only at licensed operators, rising to 95% when players who mix legal and illegal sites are counted as channelized. Those figures have been broadly stable for years.

Revenue-based channelization paints a less reassuring picture. The KSA’s corrected estimate puts that figure at 53% in H2 2025, compared with 49% in the previous report. That means nearly half of the money Dutch residents lose online now flows to unlicensed operators. It’s a meaningful gap that suggests illegal sites are capturing higher-stakes spend.

“The KSA suspects that players suffer much higher losses at illegal operators than at legal ones, because they are less protected there, or even not protected at all.”

Kansspelautoriteit, Spring 2026 Monitoring Report

The rise in the “illegal-only” player group is also notable. In H2 2025, 480,000 players used only legal sites each month. Around 30,000 played exclusively on unlicensed platforms, and 20,000 used both. Broader European analysis has warned about regulation-driven shifts toward the black market, and the Dutch numbers now offer another example.

Players aged 18 to 23 make up just 9.3% of the adult population but hold 22% of active accounts. That imbalance has persisted despite stricter rules on gambling advertising to young adults. Notably, the KSA found no visible jump in account activity between ages 23 and 24, suggesting the age-specific protections are not clearly changing behavior.

While young adults are overrepresented among active accounts, their average losses remain lower than those of older players. Their average monthly loss per used account is €34, compared with the overall average of €73. Their median loss (€33) sits close to the mean, suggesting extreme losses are rarer in this group.

Sports betting is also more popular with younger players, accounting for 23% of their GGR versus 20% for everyone else.

Since stricter player protection rules took effect in October 2024, average losses have shifted. The monthly loss per player rose slightly from €117 in H1 2025 to €124 in H2 2025. But both figures sit well below the €160 monthly average recorded in the first half of 2024, before the new rules.

Loss distribution also tells a story. Around 54% of accounts are close to break-even each month (between a €100 monthly profit and a €100 monthly loss). Another 36% lose between €100 and €1,000, and that group is now the commercial heart of the legal market.

A very small cohort, roughly 0.6% (50,000 accounts), loses more than €1,000 per month, but its share of total GGR is shrinking.

Online slot-style games remain the riskiest product. Losses per hour reached €18 on virtual slot machines, compared with €16 for other casino games. Average monthly playtime on slots was twice that of other casino games.

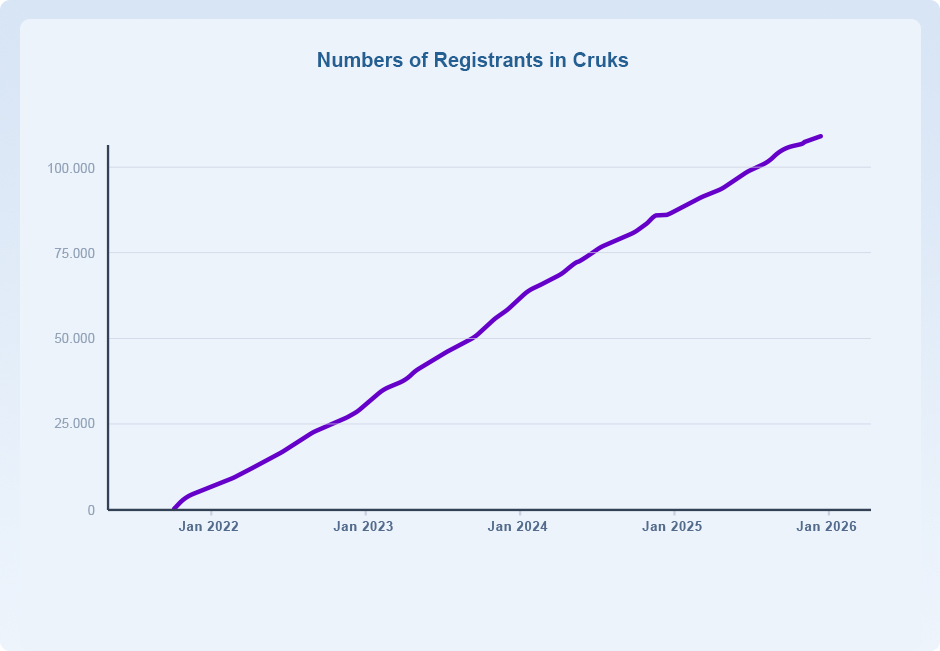

More players are turning to the Centraal Register Uitsluiting Kansspelen (Cruks), the national self-exclusion scheme. Registrations grew by about 2,149 per month on average since its launch in October 2021, reaching 111,534 by January 30, 2026.

Involuntary registrations, those triggered by operators’ duty-of-care notifications, jumped from 161 in H1 2025 to 442 in H2, after the KSA pressed licensees to flag at-risk customers.

At the same time, the problem gambling support organization, OpenOverGokken, saw website visits more than double, from 14,371 unique monthly visitors in October 2025 to 33,164 in December 2025. These trends mirror a pattern seen in other regulated European markets, where rising awareness coincides with increased use of support services.

Online gambling advertising also dropped sharply, with legal operators placing 75,000 ads per month in H2 2025, down 42% from the 129,000 monthly average in H1. Full sponsorship bans that took effect in July 2025 likely account for much of that fall.

The Dutch case is becoming a reference point for regulators weighing how far to tighten player protection rules. Losses per player are lower than they were before October 2024. Yet revenue-based channelization is slipping, multi-accounting is rising, and the illegal-only player group is slowly growing.

For regulators elsewhere in Europe, that combination raises a familiar question: at what point do safer gambling measures start to push activity toward unlicensed operators? The KSA’s next report, due in fall 2026, will test whether the Dutch market has stabilized or merely paused on its way down.