Article | 9 minutes read

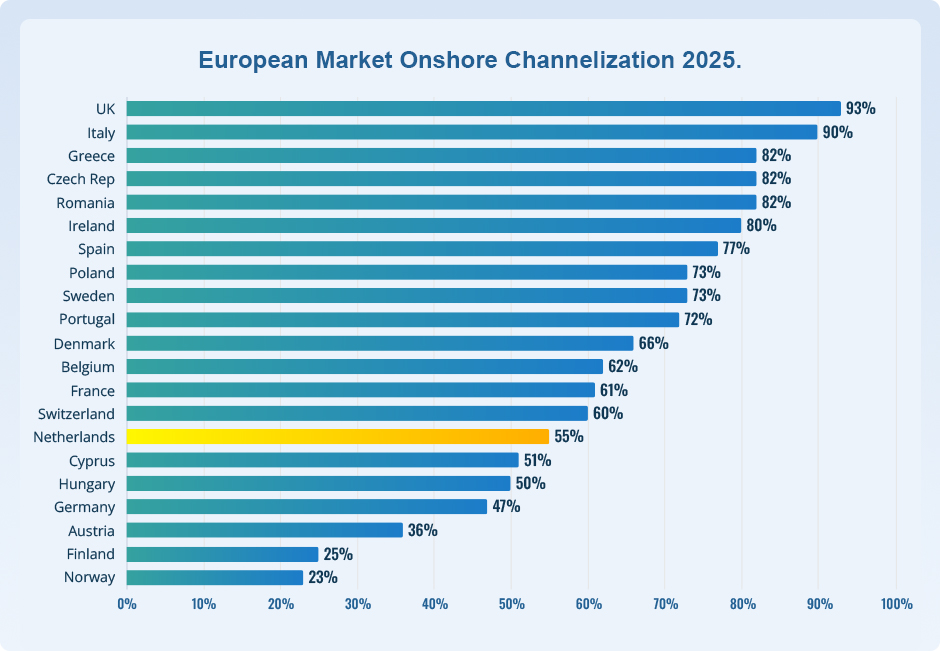

European online gambling channelization now spans a 70-percentage-point spread, from the United Kingdom at 93% to Norway at 23%. The figures from H2 Gambling Capital, presented earlier this month at the Gaming in Holland conference in Amsterdam, have sharpened a debate European regulators have had for years: when does a licensed product become so restricted that players walk away from it?

The headline finding for the host country is uncomfortable. The Netherlands sits at 55% channelization on H2’s 2025 European table, presented at the conference in June 2026. The data also reveals the reasons Dutch players give for using unlicensed casinos: the regulated offer has become less appealing than what they can find offshore.

iGaming.com CEO Prof. Dr. Andreas Ditsche shared his takeaways from the conference. He framed the figures as the clearest live evidence yet that the relationship between regulation, product attractiveness, and player migration is now measurable rather than theoretical.

H2’s onshore channelization data table shows how unevenly the European market is performing. Jurisdictions with long-established competitive markets dominate the top of the table:

The middle band is where the structural choices start to have an impact. Denmark sits at 66%, Belgium at 62%, France at 61%, and Switzerland at 60%. The Netherlands lands at 55%. That mid-table position mirrors what the Dutch gambling regulator, Kansspelautoriteit (KSA), has flagged in its own monitoring of the Dutch market for the past two reporting periods.

The bottom of the table is where the picture turns most uncomfortable for restrictive regimes:

H2 also notes that KSA-specific channelization figures for the Netherlands run “slightly lower” than its own. The two methodologies do not always align. H2 measures account-level behavior, while the KSA looks at revenue distribution. Still, both point in the same direction, and both have been moving down rather than up since the introduction of stricter Dutch deposit limits in 2024.

H2 Gambling Capital’s European channelization spread runs from 93% (UK) to 23% (Norway).

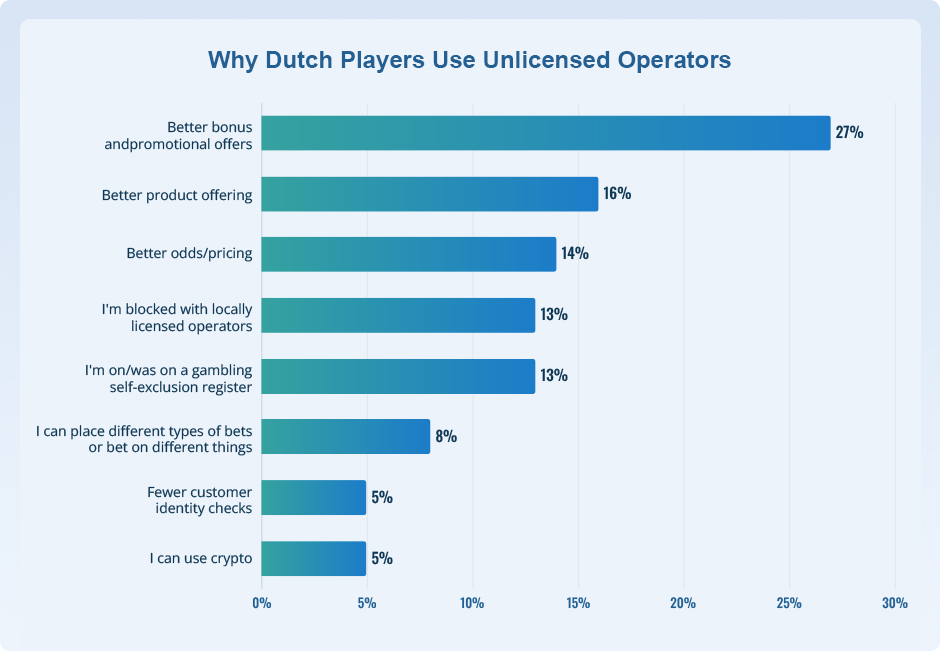

H2 Gambling Capital’s European channelization spread runs from 93% (UK) to 23% (Norway). The most striking research presented at the conference was H2’s survey-based work on player decision-making. When Dutch players who use unlicensed operators were asked why they do so, the answers were not what policymakers might expect.

The top reasons for choosing an unlicensed operator over a licensed one:

The “identity checks” and “crypto” responses sit at the very bottom of the list. The reasons players give are overwhelmingly about product preferences: bonuses, breadth of offerings, and odds. That has direct implications for how regulators design protection mechanisms. Restricting promotions or compressing operator margin tends to widen the very gap that pushes players offshore.

Prof. Dr. Andreas Ditsche, CEO of iGaming.com

H2’s data on operator choice reinforces the pattern. Asked what made them choose the operator they bet with, Dutch players ranked reputation and trustworthiness first at 17%, ease of use at 15%, brand awareness at 13%, promotions at 12%, and ease of withdrawing/depositing at 12%. Sign-up offers came in at 7%, betting odds at just 5%, and anonymity at 2%.

Trust is the strongest retention factor, and you would expect that to hold in most mature markets. But that protection only matters if the licensed market is competitive enough for players to engage with it in the first place.

Better bonuses, product offerings, and odds dominate the reasons Dutch players choose unlicensed operators.

Better bonuses, product offerings, and odds dominate the reasons Dutch players choose unlicensed operators. A second piece of H2’s player research challenges one common assumption: that consumers are simply confused about which operators are licensed. The data suggests most players know about licensing:

That last data point is important: the 62% who stay inside the licensed market are the loyal core in survey terms. It aligns with the 17% who told H2 that “reputation and trustworthiness” is their primary operator-choice factor. The leakage offshore is real, but it is concentrated within a defined cohort rather than evenly spread across the player base.

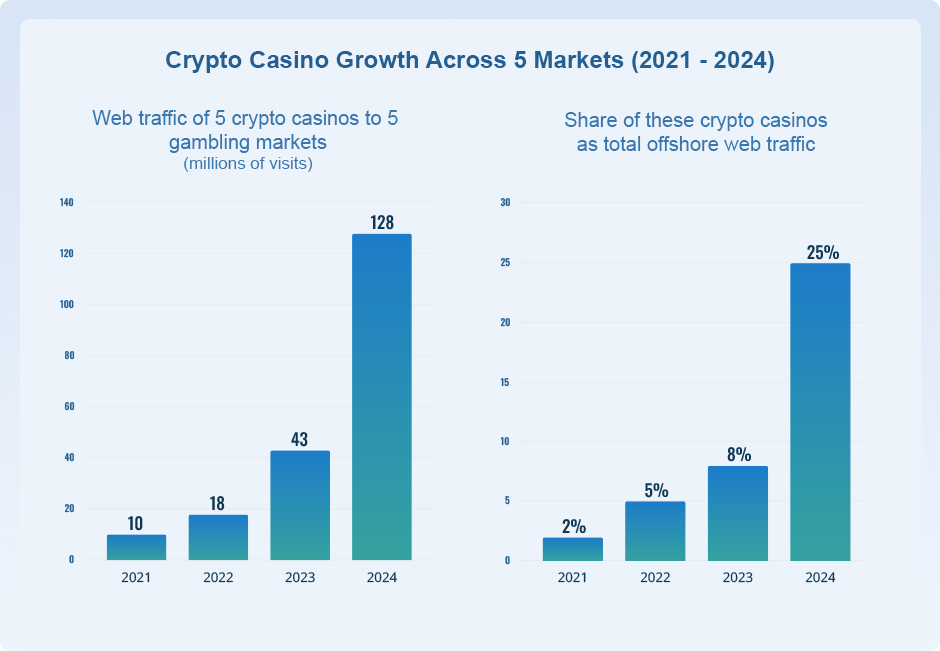

The fastest-moving trend discussed at the conference was crypto. H2’s analysis of five major crypto casinos serving five Northern European markets (Denmark, Finland, the Netherlands, Norway, Sweden) shows web traffic climbing from 10 million visits in 2021 to 128 million in 2024. That is nearly a 13-fold increase.

As a share of total offshore web traffic to these markets, crypto casinos jumped from 2% in 2021 to 25% in 2024. That growth has occurred largely out of view of national regulators, whose monitoring frameworks were not designed with crypto-rail operators in mind.

It explains why offshore player behavior can rise so quickly, even when traditional offshore brands are being blocked or fined. The structural risk is real: where crypto casinos offer faster sign-ups and less friction, the black market becomes harder to measure and easier for players to reach.

Crypto casinos have led to a significant increase in supply to offshore operators, meeting player demand.

Crypto casinos have led to a significant increase in supply to offshore operators, meeting player demand. VPN use compounds the issue. Player research found that 50% of Dutch players use a VPN at least sometimes to access unlicensed sites, with another 16% using one every time. A third of players (34%) never use a VPN. That means roughly two-thirds of the surveyed cohort have either occasional or routine experience navigating around geographic restrictions.

The Netherlands’ market findings were framed around three reinforcing factors: attractiveness, awareness, and accessibility, which overlap in a Venn diagram. Channelization increases when all three are aligned to create a competitive, licensed product that players are aware of and can access without friction. It falls when even one slips.

The Netherlands session ended with three direct conclusions:

For operators, the practical implications are unfamiliar. Pricing and product breadth, traditionally treated as commercial decisions, are now functioning as channelization tools.

For regulators currently weighing whether to tighten or loosen rules, the H2 data adds an evidence-based counterpoint. Markets with the heaviest restrictions, like Germany, Austria, and Norway, cluster in the bottom third of the channelization table.

In contrast, jurisdictions that prioritized product competitiveness alongside protection sit in the top quartile. The Dutch position at 55% is unusual not because the pattern is new, but because it is happening in real time inside a market that explicitly chose tighter rules in 2024.

Prof. Dr. Andreas Ditsche, CEO of iGaming.com

The Gaming in Holland dataset shifts the European channelization debate from theory to measured outcomes. The numbers across markets are now sharp enough to compare directly, and player-behavior research provides the “why” that channelization spreadsheets alone cannot.

The challenge for European regulators is not a lack of evidence. It is whether the evidence will be allowed to inform the next wave of policy, or whether short-term political pressure to act on visible harms will continue to widen the gap that licensed markets have spent years trying to close.

The Dutch market is a clear early example of the problem. The conference data make clear that brand reputation, not license status, is the primary anchor that keeps players in the regulated market. That only holds when the licensed product is competitive enough to keep players engaged in the first place.