Article | 9 minutes read

Two regulators are running the same experiment with the variables reversed. On July 7, 2026, the UK Gambling Commission confirmed a staged rollout of Financial Risk Assessments (FRAs) that lean on credit data and defer enforcement.

The Netherlands has run the opposite model since October 1, 2024. It requires a document-based means test that blocks deposits outright until a player proves they can afford them.

Both regulators say they are protecting players from gambling-related financial harm. Neither has produced conclusive evidence that its method works better than the alternative.

The UKGC relies on automated, data-led screening, while the KSA requires players to document their affordability. Over the next 18 months, results from both jurisdictions may show which approach offers more effective protection with the least disruption.

Both regimes target the same signal of deposits outpacing what a player can afford, but they use reverse mechanisms and enforcement stances.

| United Kingdom | Netherlands | |

|---|---|---|

| Instrument | Financial Risk Assessments, staged | Mandatory means test above deposit threshold |

| Status | Announced July 7, 2026; stage 1 first, no start date set | In force since October 1, 2024; guidance tightened July 2026 |

| Trigger, standard | £5,000 net deposits/24h (stage 1); £1,000/24h or £3,000/90 days at full rollout (age 25+) | €700 net deposits/month (age 24+) |

| Trigger, young adults | £2,500/24h (stage 1); £750/24h or £2,000/90 days at full rollout (under-25s) | €300/month (age 18–23) |

| Assessment method | Credit reference agency data, no player action | Player-supplied documents (payslips, income proof) |

| Claimed friction | 97% assessed frictionlessly; under 3% of accounts ever assessed | Manual check for every player who wants to exceed the threshold |

| If the player can’t or won’t comply | Stage 1 requires no enforcement action on results | Deposits stay blocked above the threshold |

| Enforcement posture | Deferred; “no timetable for later stages” (Helen Rhodes, UKGC) | Active; binding instruction issued to bet365; 13 “bad practices” codified |

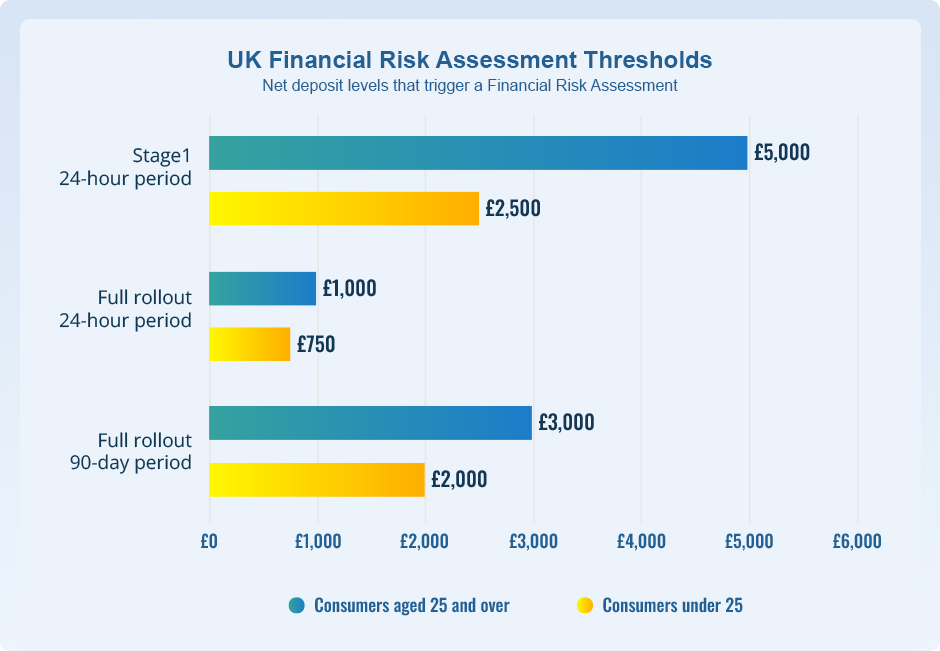

The Commission’s rollout starts narrowly. Stage one applies only to the largest operators. It reaches only customers whose net deposits exceed £5,000 in a rolling 24-hour period, a threshold the regulator says fewer than 0.5% of customers will ever cross.

Younger customers face a lower bar. Anyone under 25 triggers a check at £2,500 in 24 hours during stage one; the threshold tightens to £750 in 24 hours or £2,000 over 90 days at full rollout.

For customers 25 and over, the final thresholds drop to £1,000 in 24 hours or £3,000 over 90 days.

The Commission built its case on a pilot that ran from August 2025 to early 2026. Of the customers who crossed the spend thresholds, 97% could be assessed using credit reference agency (CRA) data alone. That comfortably beat the 80% the 2023 white paper had estimated.

Fewer than 3% of all accounts are expected to trigger an assessment once the system is fully live. Fewer than one in 1,000 will need further checks, such as open banking data or extra ID verification.

Helen Rhodes Director of Major Policy Projects and Evaluation, UK Gambling Commission

What sets this stage apart is what happens when a check flags a problem. The Commission has deliberately chosen not to enforce against operators that fail to act on a result, at least for now. Acting Chief Executive Sarah Gardner frames the trade-off as a deliberate one: data over documents.

Sarah Gardner Acting Chief Executive Officer, UK Gambling Commission

That deferred-enforcement stance fits a pattern the UKGC FVC findings already flagged: the Commission moving carefully, with open questions doing most of the work.

The Betting and Gaming Council (BGC) isn’t convinced the 97% figure tells the full story. Chief Executive Grainne Hurst said the pilot “exposed inconsistencies in the information returned by credit reference agencies, with the same customer potentially receiving different outcomes depending on the provider.”

The Dutch model has a hard threshold rather than a probability score. Since October 2024, players wanting to deposit above €300 a month (ages 18–23) or €700 a month (ages 24 and over) must first pass a documented means test.

Below those levels, nothing changes. Above them, deposits stay blocked until the paperwork clears. Those figures are thresholds, not caps. A player can deposit more than €700 a month, but only after proving, on paper, that they can afford to.

Guidance tightened again this month. The KSA’s revised good and bad practices document, published in early July 2026, closes ambiguities in the original February 2025 guidance. Deposit limits must now be calculated from “structural,” meaning recurring, income only.

Savings, business assets, home equity, and one-off payments like bonuses or gifts no longer count toward a player’s limit. The KSA said operators had misread the earlier wording and inflated deposit limits by including exactly those items.

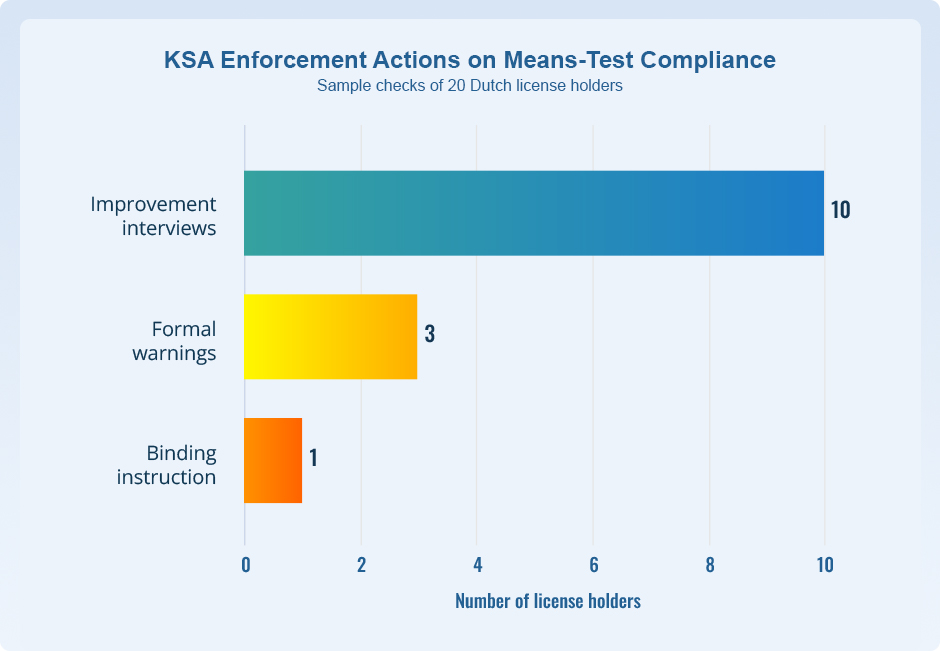

Following the original February 2025 guidance, the regulator conducted follow-up research. Sample checks of 20 license holders revealed persistent non-compliance, prompting 10 improvement interviews, 3 formal warnings, and 1 binding instruction. The 13 documented “bad practices” include accepting self-declared income without verification and applying bonus restrictions for less than the mandatory 30-day period after a deposit-limit intervention.

From the 20 operators checked, bet365 is the binding-instruction case. The KSA found the operator relied on self-completed player questionnaires to assess affordability, a method it had explicitly warned against in early 2025.

The regulator also found that bet365 miscalculated deposit limits, in some cases allowing players to deposit anywhere from 31.8% to more than 100% of their assessed monthly net income. The operator disputed the allegations and was given four weeks to comply.

Public appetite for the regime appears to be holding up. A 1,507-respondent study, first published in October 2025 and cited again in the KSA’s July 2026 guidance update, found that support for deposit limits rose from 76% two years earlier to 82%.

The UK’s model is largely untested at the national scale, and its enforcement-free stage one may not yet protect anyone who fails a check. A BGC-commissioned poll found that 65% of UK bettors would refuse to hand over financial documents such as bank statements or payslips if asked. That resistance is a major reason the Commission built a data-first system rather than a document-first one.

The Dutch friction is real, and the regulator’s own numbers back it up. Channelization measured by gross gaming revenue fell to 53% in the second half of 2025. Player-based channelization held up better, ranging from 91% to 95%, meaning most players stayed registered even as spend drifted elsewhere.

Trade press covering the KSA’s own figures has tied that slide to a combination of factors: a 2025 gambling-tax increase, alongside tighter deposit and means-test rules, not to affordability checks in isolation.

None of this proves that affordability checks push players offshore on their own. The EU’s illegal online gambling market, valued at €91.6 billion in 2025 by the European Casino Association, grew roughly 14% on the year and cost an estimated €22.9 billion in lost tax revenue. It has been growing across markets with very different rules.

The Netherlands actively enforces and accepts the channelization risk that comes with friction. The UK avoids friction in stage one and, for now, avoids enforcement too. Both are conscious trade-offs, not accidents, a version of the overregulation-versus-channelization tension that keeps resurfacing across Europe’s gambling markets.

Across Europe, different markets have taken varied approaches to player protection limits:

Each of those markets is watching how far channelization can bend before players stop registering with licensed operators altogether. It’s a question that has split European regulators for years, with no shared standard in sight.

The UK’s premise is that friction, not spending, is what pushes players toward unlicensed sites. For the Netherlands, friction is the price of catching financial harm before it compounds. Both bets rest on the same underlying question: how much verification can a regulated market ask for before players start looking elsewhere to play?

The UK’s model depends on infrastructure it hasn’t fully built yet: data-sharing pipelines between operators and credit reference agencies that need to work consistently before thresholds tighten further. That’s an operational problem as much as a policy one, and it will shape how quickly later FRA stages can roll out.

Two years of Dutch channelization data and the UK’s first full year of live FRAs should settle more of this than either regulator’s current rhetoric can.

Until then, players in both markets have direct routes to support. In the UK: GamCare, GamStop, and the National Gambling Helpline (0808 8020 133). In the Netherlands: OpenOverGokken, Cruks, and AGOG.